Structured payment plans are a practical way for businesses to manage debt without filing for bankruptcy. These agreements allow companies to renegotiate payment terms, such as reducing interest rates, extending repayment periods, or lowering monthly payments, to align with their financial situation. By avoiding bankruptcy, businesses can maintain operations, protect their reputation, and preserve relationships with creditors.

Key Points:

- What They Are: Agreements between debtors and creditors to revise debt terms.

- Benefits: Avoid bankruptcy, improve cash flow, and maintain creditor trust.

- Challenges: Legal risks, administrative workload, and potential tax implications.

- Steps to Create a Plan:

- Assess financial health and gather documents.

- Negotiate with creditors for adjusted terms.

- Monitor compliance and adjust as needed.

Platforms like Urgent Exits streamline the process by connecting businesses with experts and providing tools for negotiation, documentation, and monitoring. These digital solutions simplify debt workouts, making recovery more efficient and accessible.

Key Components of Structured Payment Plans

When it comes to structured payment plans, getting the details right is essential for both parties involved. A well-thought-out plan not only helps businesses manage debt but also ensures creditors feel secure about repayment. Let’s dive into the critical elements that make these plans work smoothly.

Core Elements of a Payment Plan

The payment schedule is the backbone of any structured payment plan. It lays out a clear timeline for payments, tailored to the debtor’s financial situation. For instance, a seasonal retailer might negotiate smaller payments during slower months and larger ones during busy holiday seasons. This schedule should specify exact dates, amounts, and how often payments are made – whether monthly, quarterly, or tied to revenue cycles.

Interest rate adjustments can make or break an agreement. Creditors might lower interest rates to help struggling businesses, like reducing an 8% rate to 4%. In some cases, agreements might shift from variable to fixed rates or even pause interest accrual temporarily, giving businesses the breathing room they need to recover.

Grace periods are another critical component, offering temporary relief when businesses face unexpected challenges. These periods, which can range from 30 days to several months, allow companies to focus on stabilizing operations without the immediate stress of payments. Negotiating a grace period can help maintain trust between both parties while giving the business time to regroup.

Default provisions are essential for clarity. These terms outline what happens if payments are missed, defining what constitutes a default and the resulting consequences. Having these details spelled out helps avoid confusion and ensures both sides know what to expect.

Other elements might include collateral arrangements or modified covenants to reflect the debtor’s current financial situation. In some cases, creditors may even waive previous defaults, giving the business a fresh start.

Legal and Documentation Requirements

For a structured payment plan to hold up legally, it must be clearly documented in writing. This process involves drafting agreements that comply with U.S. federal contract law and, where relevant, the Uniform Commercial Code (UCC).

The written agreement should cover everything – from the payment schedule to default provisions – and must be signed by authorized representatives from all parties. If collateral is part of the deal, proper documentation of those security interests is crucial. Additionally, state-specific laws may require extra steps, such as consumer protection measures that influence how these plans are structured and recorded.

Thorough documentation serves multiple purposes: it enforces the agreement, provides evidence in case of disputes, ensures compliance, and even assists with tax reporting. Typical documents include the main payment plan, amendments to original loan agreements, security agreements for collateral, and records of the negotiation process.

"Legal documentation is crucial in structured payment plans to ensure that all parties understand their obligations and rights, which minimizes the risk of future disputes." – John Smith, Bankruptcy Attorney

Enlisting the help of experienced legal counsel during this phase is highly advisable. Attorneys and restructuring experts ensure the agreement meets legal standards, minimize errors, and increase the chances of creditor approval. They also provide insights into tax and regulatory considerations that businesses might overlook.

Proper documentation is the foundation of a successful payment plan. Informal or poorly documented agreements can lead to misunderstandings, unenforceable terms, and a greater risk of default – defeating the purpose of the plan.

Services like Urgent Exits connect businesses with restructuring professionals, attorneys, and consultants, ensuring that all agreements are legally sound. Having access to this kind of expertise is key to creating arrangements that protect everyone involved.

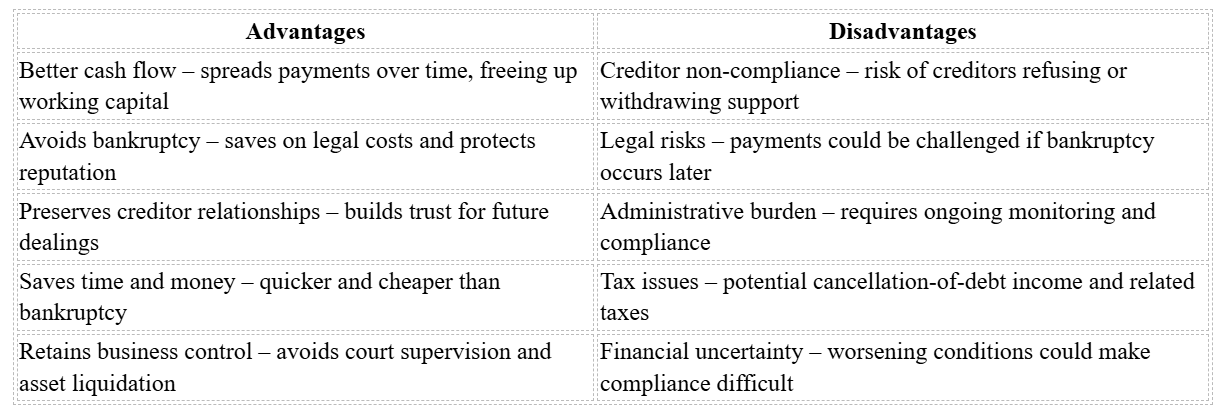

Benefits and Challenges of Structured Payment Plans

Structured payment plans can be a lifeline for struggling businesses, offering a way to manage debt while keeping operations afloat. However, they also come with hurdles that require careful planning and execution. These plans are an essential tool in debt management, balancing the need for financial relief with the risks involved.

Advantages for Distressed Businesses

One of the most notable advantages is better cash flow management. By spreading out payments and reducing monthly obligations, businesses can free up working capital for day-to-day operations. For example, a small business might renegotiate its loan terms to lower interest rates and extend repayment periods, easing its financial strain.

Another key benefit is avoiding the high costs and reputational damage associated with bankruptcy. Structured payment plans allow businesses to renegotiate debt terms – whether by lowering payments, reducing interest rates, or extending deadlines – giving them the breathing room needed to stay afloat without resorting to legal proceedings .

These plans also help maintain strong relationships with creditors. Demonstrating a willingness to cooperate through a structured plan can build trust, which may lead to better terms in future negotiations. For instance, a startup successfully avoided bankruptcy by using a workout agreement to manage its debts, preserving both its operations and creditor confidence.

Beyond these advantages, structured payment plans are often quicker and less expensive than formal bankruptcy processes. This has become even more appealing after regulatory changes made bankruptcy relief harder to obtain . Despite these benefits, businesses must navigate several challenges to implement these plans effectively.

Common Challenges

While structured payment plans offer clear benefits, they are not without difficulties. One major challenge is creditor non-compliance. If key creditors refuse to participate or later back out, the plan’s success could be at risk, potentially leading to bankruptcy or legal disputes. Reaching an agreement that satisfies enough creditors – without requiring all of them to agree to identical terms – is critical .

Legal risks are another concern. Payments or security interests arranged through a workout could be challenged later if the business files for bankruptcy. Issues like preference or fraudulent transfer claims can complicate matters. Additionally, tax consequences may arise. For example, if a lender reduces a business’s principal debt from $5 million to $4 million, the $1 million difference might be considered taxable income.

The administrative workload involved in maintaining these plans can also be overwhelming. Businesses need to dedicate time and resources to regular reporting, monitoring, and updating agreements. This often requires hiring staff, investing in financial management tools, or seeking professional advice. The complexity increases when additional factors, like subordination agreements, come into play .

Comparison Table: Pros and Cons

For businesses weighing structured payment plans, careful consideration is essential. Open communication with creditors, a detailed financial review before negotiations, and expert legal and financial advice can help craft realistic agreements. Regular updates and adjustments, aligned with the business’s changing circumstances, are also crucial for long-term success .

Platforms like Urgent Exits (https://urgentexits.com) can be a valuable resource, connecting businesses with restructuring professionals, attorneys, and consultants. These experts can assist in negotiating complex payment arrangements or exploring alternatives, such as selling the business to resolve debt challenges.

Steps to Negotiate a Structured Payment Plan

Negotiating a structured payment plan requires thoughtful preparation and a step-by-step approach. It involves three key phases that work together to create a manageable solution for addressing debt.

Initial Financial Assessment

Before reaching out to creditors, it’s essential to get a clear picture of your financial situation. This step establishes your credibility and helps you approach negotiations with confidence.

Start by gathering 12–24 months’ worth of financial records – balance sheets, income statements, cash flow statements, and tax returns. Create a detailed list of all your debts, including the names of creditors, the amounts owed, interest rates, payment schedules, and any collateral arrangements.

Next, prepare conservative cash flow projections for the next 12–18 months, factoring in seasonal trends and potential cost fluctuations. This will give you a realistic view of your financial capacity.

Identify any current or potential defaults, as this will help you prioritize which creditors to address first. If possible, consult a financial advisor or accountant to review your situation. Their expertise not only adds credibility but also ensures you’ve accounted for all critical financial details, including potential tax implications.

With this groundwork in place, you’ll be ready to approach creditors with a clear and organized plan.

Engaging Creditors and Drafting Agreements

Once your financial assessment is complete, reach out to creditors individually with a well-documented proposal. Your proposal should include an overview of your financial situation and specific changes you’re requesting – such as extending repayment terms, lowering interest rates, reducing monthly payments, or temporarily deferring payments.

Support your request with financial documents and cash flow forecasts. Demonstrating your commitment to resolving the situation increases the chances that creditors will be open to working with you. Highlight that structured payment plans often allow creditors to recover more than they would through bankruptcy, making it a mutually beneficial option.

Work with your creditors to amend existing loan agreements or draft new forbearance and waiver agreements. These documents should comply with state contract laws and the Uniform Commercial Code (UCC), particularly Article 9 for secured transactions. Clearly outline payment amounts, due dates, interest rates, and any collateral arrangements. Don’t forget to address potential tax consequences, such as Cancellation of Debt (COD) income if the principal is reduced. Include provisions for dispute resolution and flexibility in case circumstances change.

Monitoring and Adjustments

After agreements are finalized, the work doesn’t stop. Ongoing monitoring and adjustments are crucial to staying on track.

Set up systems to track your compliance with the terms of the agreement. Regular financial reporting will help you monitor cash flow against your projections and ensure you meet payment deadlines. Accounting software can be a valuable tool to prevent missed payments and flag potential issues early.

Schedule regular check-ins with creditors to discuss progress and make adjustments if necessary. These conversations help maintain trust and provide an opportunity to renegotiate terms if your financial situation changes. For example, you might need seasonal payment adjustments or modifications based on specific financial metrics.

If your financial circumstances improve or worsen, notify your creditors promptly and provide updated financial information. Open communication reinforces your commitment and increases the likelihood of securing additional flexibility if needed.

For additional support, consider platforms like Urgent Exits (https://urgentexits.com), which connect you with experienced restructuring professionals, attorneys, and consultants. These experts can help ensure your agreements meet legal requirements and provide ongoing guidance as your situation evolves.

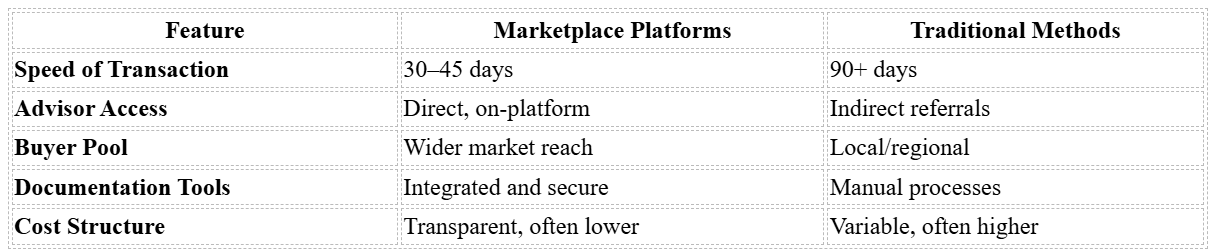

Marketplace Solutions for Structured Payment Plans

Expanding on earlier negotiation strategies, digital marketplaces now offer a smoother way to access structured payment plans. These platforms simplify the process of negotiating, implementing, and monitoring payment plans, presenting a modern alternative to traditional debt resolution methods.

Using Urgent Exits for Debt Workouts

Urgent Exits is a specialized marketplace designed to connect struggling businesses with motivated buyers and experienced restructuring professionals. It speeds up debt workout transactions by providing a direct and efficient platform for businesses under financial strain. Unlike traditional brokers, who may shy away from complex cases, Urgent Exits welcomes these challenges, offering immediate access to a network of professionals and buyers ready to assist.

The platform’s listing process is quick, taking just minutes to complete. This allows businesses to present their financial situation to a focused audience without unnecessary delays. By moving the process online, Urgent Exits significantly shortens the time typically required for such transactions.

One standout feature of Urgent Exits is its extensive network of professionals, including appraisers, consultants, lenders, accountants, lawyers, auctioneers, and liquidators. These experts help businesses evaluate their financial standing, draft legally compliant payment plans, and provide ongoing support. The platform’s secure communication tools, such as messaging and document sharing, allow all parties to collaborate directly. This eliminates the delays and miscommunications that often arise when multiple intermediaries are involved. Businesses can share financial documents, receive feedback on payment plans, and negotiate terms – all in real time.

For companies considering restructuring alongside potential asset sales, Urgent Exits supports both approaches. This dual functionality helps businesses tackle debt while exploring opportunities to sell assets, creating a streamlined process with practical benefits.

Practical Benefits for Distressed Businesses

Marketplace platforms offer more than just convenience – they deliver tangible advantages for businesses navigating financial difficulties. For instance, performance tracking tools allow businesses to monitor their compliance with payment plans and address potential issues before they escalate.

Direct access to advisors is another critical benefit. Instead of spending weeks searching for qualified professionals, businesses can instantly connect with experts who bring valuable insights to the table. These professionals assist in crafting legally sound agreements and ensuring compliance throughout the process.

Transparency is also a key feature of these platforms. Specialized tools allow for real-time adjustments and clear documentation tracking, creating a transparent process that benefits both businesses and creditors. This clarity often fosters trust and can lead to more flexible terms.

Marketplace platforms also enhance communication between buyers and sellers, enabling flexible negotiations that might not be possible through traditional methods. This often results in creative restructuring solutions tailored to the unique needs of distressed businesses.

For businesses that successfully adopt structured payment plans through these platforms, ongoing monitoring tools provide added reassurance. Real-time updates and financial health indicators ensure compliance with agreements and quickly highlight any changes that may require adjustments.

Additionally, platforms like Urgent Exits offer educational resources that are especially helpful for business owners new to debt workouts. These guides break down the process, helping users prepare documentation, understand their options, and communicate effectively with creditors and advisors. This support can make a challenging situation much easier to navigate.

Conclusion and Key Takeaways

Structured Payment Plans: A Practical Lifeline

Structured payment plans can be a game-changer for businesses grappling with significant debt. These arrangements provide a clear pathway to financial recovery, helping companies avoid the harsh reality of bankruptcy. By tailoring repayment schedules to align with a business’s cash flow, they offer much-needed breathing room to regain stability.

Research highlights their effectiveness, with recovery chances improving by up to 60% and a notable reduction in bankruptcy risk. For instance, a business owner managed to secure a 20-year repayment extension with reduced interest rates – starting at 4.5% for two years, then adjusting to 5.5%. This adjustment brought monthly payments down to $3,164, allowing the business to stabilize operations.

The success of these plans largely depends on early action. Engaging creditors before defaulting and conducting a thorough financial review are crucial steps. Businesses that take a proactive approach often secure better terms and maintain stronger relationships with lenders. Regular reviews and adjustments further ensure that these plans remain practical and effective.

With these benefits in mind, digital tools are now playing a key role in making debt recovery even more efficient.

The Role of Modern Marketplaces

The advantages of structured payment plans are amplified by the rise of specialized digital platforms. These tools have revolutionized how businesses handle debt workouts. Take Urgent Exits, for example – a platform designed to connect struggling businesses with buyers, advisors, and restructuring experts who specialize in financial recovery.

Urgent Exits goes beyond simple business listings. It offers access to a network of professionals, including appraisers, consultants, accountants, lawyers, and liquidators. This streamlined access to expertise helps businesses avoid delays and find tailored solutions for their unique challenges.

For companies exploring structured payment plans, platforms like Urgent Exits enhance the process with features like secure document sharing, real-time feedback, and performance tracking. These tools bring transparency and efficiency to what can otherwise be a daunting process.

Ultimately, structured payment plans thrive when paired with the right resources and expert guidance. Digital platforms expand access to these critical tools, providing businesses with the support they need to navigate financial difficulties and emerge stronger. By integrating structured payment plans with modern technology, businesses can take a proactive approach to overcoming financial challenges.

FAQs

What steps can businesses take to comply with structured payment plans and avoid legal complications?

To stick to structured payment plans and avoid legal trouble, businesses need to start with clear, well-documented agreements. These should spell out payment terms, deadlines, and any penalties for falling short. Keeping everything transparent and maintaining detailed records helps ensure accountability and keeps everyone on the same page.

Partnering with financial and legal advisors is another smart move. They can confirm that the payment plan aligns with relevant laws and regulations. Regularly checking your business’s financial situation and tweaking the plan when needed can help avoid missed payments and disputes. Staying in touch with creditors and addressing concerns quickly builds trust and keeps the process running smoothly.

What tax considerations should businesses keep in mind when setting up a structured payment plan?

When setting up a structured payment plan, it’s crucial for businesses to consider potential tax consequences. For example, if part of a debt is forgiven through a workout plan, the forgiven amount may be treated as taxable income. This is referred to as cancellation of debt (COD) income, unless certain exclusions under IRS regulations apply.

Equally important is structuring payments in a way that fits your cash flow while keeping tax obligations in mind. Working with a tax professional or advisor can provide valuable guidance, helping you manage these complexities and steer clear of any unforeseen tax issues.

How can platforms like Urgent Exits simplify negotiating and managing structured payment plans for distressed businesses?

Platforms like Urgent Exits simplify the process of crafting and managing structured payment plans by connecting sellers of struggling businesses with interested buyers and professional advisors. This setup helps speed up negotiations and provides solutions that align with everyone’s needs.

Through its centralized marketplace, Urgent Exits enables sellers to list their businesses quickly and efficiently, giving buyers access to potentially undervalued opportunities. At the same time, advisors – such as accountants, consultants, and legal professionals – can connect with clients to assist in restructuring efforts and payment plan discussions. This collaborative model offers critical support for businesses facing financial hurdles.